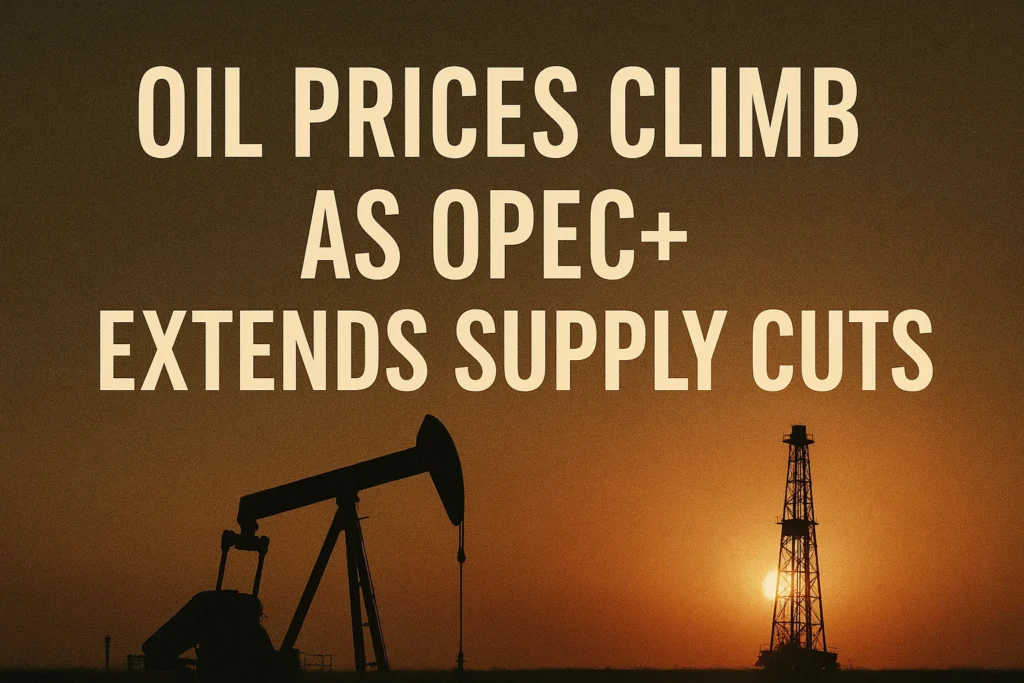

The opulent boardrooms of Vienna’s OPEC Secretariat are a world away from the daily commute, the weekly grocery run, or the family budget meeting around a kitchen table. Yet, the decisions made within them are inextricably linked to these mundane realities. In the summer of 2024, a coalition of the world’s most powerful oil-producing nations announced a decision that would resonate for years: the extension of deep supply cuts into 2026. This was not merely a footnote in the business section; it was a seismic event in the global economic landscape, a deliberate move that would touch the lives of billions, from the metropolises of the developed world to the most vulnerable emerging economies. This is the story of that decision, the complex machinery behind it, and the profound, often personal, consequences it unleashes.

The Invisible Hand from Vienna: A Decision That Moved the World

The air in the Austrian capital is often thick with the grandeur of history and the soft melodies of classical music. But on one particular day, the atmosphere in a high-security boardroom was charged with a different kind of energy—the kind that moves markets and defines the destinies of nations. Ministers from the world’s most influential oil-producing countries sat around a large, polished table, not to compose a symphony, but to orchestrate a global economic maneuver. They spoke in a language of millions of barrels per day, a vocabulary alien to most. Yet, the consensus they reached—a collective decision to keep millions of barrels of crude oil off the market—would soon reverberate far beyond their quiet chambers. This was not merely an administrative announcement; it was a deliberate act of market intervention, a geopolitical chess move whose consequences would ripple through the supply chains of every industry, the balance sheets of every corporation, and ultimately, the daily financial reality of billions of people. This is the story of how an unseen decision in a distant city connects directly to the price of your commute, the cost of your heating, and the stability of your household budget.

The Anatomy of OPEC+: Understanding the World’s Most Powerful Energy Cartel

To comprehend the shockwaves, one must first understand the earthquake. OPEC+ is not a monolithic corporation but a complex and often fragile alliance of sovereign nations with a shared economic interest: managing the global supply of crude oil to ensure price stability and, crucially, revenue adequacy for their state budgets.

The Foundation: OPEC Itself

The Organization of the Petroleum Exporting Countries (OPEC) was founded in Baghdad in 1960 by Iran, Iraq, Kuwait, Saudi Arabia, and Venezuela. Their goal was revolutionary: to coordinate petroleum policies and secure a fair return for their natural resources, wresting control from the “Seven Sisters” – the powerful Western oil conglomerates that then dominated the industry. The core principle was, and remains, collective action. Today, OPEC has 13 member countries: Algeria, Angola, Congo, Equatorial Guinea, Gabon, Iran, Iraq, Kuwait, Libya, Nigeria, Saudi Arabia, the United Arab Emirates, and Venezuela. Together, they hold the vast majority of the world’s proven oil reserves.

The “+” Factor: A Broader, More Powerful Coalition

The “+” signifies a crucial evolution. In 2016, with oil prices languishing below $30 a barrel, a paradigm shift occurred. OPEC, led by Saudi Arabia, realized it could no longer manage the market alone. The rise of new producers, most notably the United States shale revolution, had diluted its influence. The solution was to bring non-OPEC producers into a formal agreement. Russia, the world’s second-largest oil producer, became the cornerstone of this new alliance, dubbed OPEC+. Other significant “+” members include Azerbaijan, Bahrain, Brunei, Kazakhstan, Malaysia, Mexico, Oman, South Sudan, and Sudan.

This expanded group controls an astonishing over 40% of global crude oil production and possesses an even larger share of proven reserves. This collective muscle gives them unparalleled power to influence the price of the world’s most traded commodity. Their primary tool is production quotas—agreed-upon limits on how much oil each member can pump. By collectively turning the tap up or down, they can flood the market to drive prices down (a tactic rarely used) or, as in the current case, constrict supply to drive prices up.

The Precipice: The Global Economic Context of the 2024 Decision

The OPEC+ meeting in June 2024 did not occur in a vacuum. Ministers arrived in Vienna facing a perfect storm of competing pressures, making their decision one of the most consequential in the group’s history.

The Inflationary Ghost

For two years, the world’s major economies had been battling the highest inflation rates in a generation. Central banks, led by the U.S. Federal Reserve and the European Central Bank, had embarked on an aggressive campaign of interest rate hikes. The goal was to cool overheated economies by making borrowing more expensive, thereby reducing demand and bringing prices down. This “tight monetary policy” was a delicate and painful operation, risking recession and unemployment. Energy prices are a core component of inflation. OPEC+ was acutely aware that any action to significantly raise oil prices could undermine this global fight, forcing even more aggressive rate hikes and potentially triggering a deep economic downturn, which would, in turn, crush oil demand.

The Demand Dilemma

The post-COVID recovery in oil demand had been uneven. While air travel and mobility in the West had largely recovered, China’s economic rebound, a key engine of global oil growth, was sputtering. Property market crises and weak consumer spending meant the world’s largest oil importer was not consuming as much as predicted. Meanwhile, the relentless long-term trend of electrification and efficiency gains was slowly eroding oil’s dominance in the transportation sector. OPEC+ had to balance its desire for high prices with the fear of killing demand.

The Geopolitical Fault Lines

The alliance itself was under strain. The war in Ukraine had placed Russia, a key OPEC+ partner, under severe Western sanctions. While Russian oil continued to flow, it was often sold at a discount to new markets like India and China. Furthermore, the close cooperation between Saudi Arabia and Russia, despite the latter’s pariah status in the West, was a constant source of geopolitical tension. The U.S., a close Saudi ally for decades, had repeatedly called on the Kingdom to increase production to help lower global prices and squeeze Russian revenue. Saudi Arabia’s refusal to break from Moscow signaled a significant realignment in global politics.

It was on this knife’s edge that the ministers made their calculus. The decision to extend cuts was a bold bet that their need for fiscal revenue outweighed the risks of exacerbating global inflation and accelerating the transition away from their primary commodity.

The Vienna Accord: A Deep Dive into the Mechanics of the Supply Cuts

The announcement from Vienna was a masterclass in market management, featuring a multi-layered, phased approach designed to provide long-term guidance while retaining flexibility.

1. The “Voluntary” Cuts: The Inner Circle’s Commitment

A subset of OPEC+ members, led by Saudi Arabia and Russia, had previously implemented additional, deeper cuts beyond their formal group quota. These were framed as “voluntary” but were, in fact, highly coordinated. The June 2024 decision extended this specific cut of 2.2 million barrels per day (bpd). To grasp this scale, consider that 2.2 million bpd is more than the entire oil output of a major producer like Nigeria or Qatar. This extension was set to last until the end of the third quarter of 2024 (September 2024).

2. The Phased “Unwinding”: A Cautious Return

The most revealing part of the agreement was the plan for after September 2024. The group did not promise to simply restore this oil. Instead, they outlined a painfully gradual, conditional return of these barrels to the market. The plan was to add the supply back incrementally between October 2024 and September 2025—a full year for a return to the status quo. Crucially, this plan was caveated with a clear condition: it was “subject to market conditions.” This meant OPEC+ reserved the right to pause or reverse the process entirely if prices began to weaken during that period.

3. The Formal Group Cut: The Foundation of the Strategy

Separate from the “voluntary” cuts, the entire OPEC+ alliance had already been adhering to a broader production cut of 3.66 million bpd. This cut was now officially extended until the end of 2025. This provided a solid, high-price floor for the medium term.

The Masterstroke: Certainty and Flexibility

The brilliance of this structure was its communication to the market. It provided certainty—traders now knew significant volumes of oil would be withheld for at least another year and a half. But it also provided OPEC+ with maximum flexibility. They could respond to any economic shock or demand surge without having to call an emergency meeting. They had built a automatic stabilizer into their agreement. The message was clear: we are in control for the long haul.

The Market Responds: Traders, Algorithms, and the Immediate Price Surge

In the digital age, global markets operate at the speed of light. The OPEC+ communiqué was instantly dissected by analysts, interpreted by algorithms, and acted upon by traders in financial hubs across the globe.

The reaction was immediate and decisive. Brent Crude, the international benchmark, jumped over 2% within hours. West Texas Intermediate (WTI), the U.S. benchmark, followed suit. In the world of oil futures, where contracts worth billions of dollars change hands every minute, such a move is significant. This was not a fleeting spike; it represented a fundamental repricing of the market’s expectations for the next two years.

The surge was driven by two key factors:

- The Element of Surprise: While an extension was widely expected, its duration and the detailed plan for a phased return were more assertive than many analysts had predicted. The market had to quickly adjust to a new reality of tighter-than-anticipated supplies.

- The “Term Structure” Shift: A critical indicator in oil markets is the difference in price between oil for immediate delivery and oil for delivery in the future (known as the “forward curve”). The OPEC+ announcement caused the price of near-term contracts to rise faster than longer-dated ones. This created a market condition known as “backwardation,” where prompt oil is more expensive than future oil. This is a classic sign of a tight physical market and is typically interpreted by traders as a bullish signal, encouraging further buying.

This initial price jump set the tone, establishing a new, higher trading range that would persist, creating a higher baseline cost for everything derived from crude oil.

The Domino Effect: Tracing the Path from the Oil Barrel to Your Everyday Life

The price of a barrel of oil is an abstract number to most people. Its real-world impact is felt through a long and intricate chain of cause and effect—a domino effect that travels from the futures market to the daily realities of household budgets.

Domino 1: The Refinery Gate

Crude oil is useless in its raw form. It must be transported to massive industrial complexes called refineries, where it is heated and distilled into its component parts through a process called fractional distillation. The main products are:

- Gasoline (for cars)

- Diesel (for trucks, ships, and farm equipment)

- Jet Fuel (for aviation)

- Heating Oil

- Heavier products used for asphalt, lubricants, and petrochemicals.

When the price of the input (crude) rises, the cost of producing these outputs rises in lockstep. Refineries, which operate on thin margins, immediately pass these increased costs on to fuel distributors.

Domino 2: The Fuel Distributor

Fuel distributors buy refined products in bulk and sell them to retail outlets: gas stations, truck stops, and airlines. Their contracts are often directly tied to the daily fluctuations of the futures market. A rise in their wholesale purchase price is instantly reflected in the prices they charge their customers.

Domino 3: The Retail Pump and Beyond

This is the most visible domino for the consumer. The price at the gas station sign changes, sometimes daily. A family filling up their SUV feels the impact directly. But the ripple extends far beyond the pump.

- The Trucking Fleet: The entire global logistics network runs on diesel. When the price of diesel rises, the cost of moving every single good—from food and clothing to electronics and building materials—increases. Trucking companies add fuel surcharges to their invoices.

- The Farm: Modern agriculture is energy-intensive. Diesel powers tractors and harvesters. Natural gas is a key ingredient in fertilizer. Higher energy costs make it more expensive to grow food.

- The Airline: Jet fuel is often an airline’s single largest expense. To offset higher costs, airlines raise ticket prices and add fees for baggage and services.

- The Factory and the Store: Manufacturers face higher costs for power and for the plastic and petrochemical components in their products. Retailers then face higher costs from their suppliers and their own shipping bills. To maintain profitability, they raise shelf prices.

This is how a decision in Vienna translates to a higher bill at the grocery store. It is a textbook example of cost-push inflation, where increased costs of production lead to a general increase in the price level of goods and services throughout the economy.

The Inflationary Vortex: Central Banks in a Quandary

The domino effect places the world’s central banks in an extremely difficult position. Their mandate is to maintain price stability—to keep inflation low and predictable. The primary tool they use is interest rates.

The Mechanism: By raising interest rates, a central bank like the U.S. Federal Reserve makes borrowing money more expensive for consumers (mortgages, car loans, credit cards) and businesses (expansion loans, inventory financing). This cools down economic activity, reduces demand, and, in theory, brings prices back down.

The OPEC+ Complication: The inflation caused by higher oil prices is not due to an overheated economy where everyone is spending too much. It is an external shock to the cost side of the economy. This creates a terrible dilemma for central bankers, often called “stagflation risk”—the prospect of stagnant economic growth combined with high inflation.

If they respond to OPEC+-driven inflation by raising interest rates aggressively, they risk triggering a severe recession by crushing demand in sectors already suffering from high costs. Millions could lose their jobs. However, if they do nothing, inflation expectations could become “unanchored,” leading to a wage-price spiral where workers demand higher pay to keep up with costs, and businesses raise prices further to pay those wages.

The OPEC+ decision effectively forces central banks into a “higher for longer” interest rate policy. It removes their flexibility and increases the pain of the economic medicine they must administer. The burden of this is borne by homeowners with adjustable-rate mortgages, small businesses seeking loans, and anyone with debt.

Winners and Losers: A Tale of Two Global Economies

The extended supply cuts create a stark divide between the producers and consumers of the world, reshaping national fortunes and individual livelihoods.

The Winners: Petrostates and Their Balance Sheets

For the OPEC+ nations, this is a strategic victory essential for their fiscal survival. These countries rely on oil revenue to fund their governments, often providing generous subsidies and public sector jobs to their populations in lieu of taxation.

- Saudi Arabia: The de facto leader needs an oil price well above $90 per barrel to fund its ambitious “Vision 2030,” a plan to diversify its economy away from oil and build mega-projects like the futuristic city Neom. High prices are the fuel for this transformation.

- Russia: For a nation under severe financial sanctions, high oil prices are a geopolitical lifeline. Every extra dollar per barrel provides hundreds of millions of dollars for the state treasury, helping to fund its war effort in Ukraine and stabilize its domestic economy against Western pressure.

- The Gulf States (UAE, Kuwait, Iraq): These nations have economies almost entirely dependent on hydrocarbon revenue. Sustained high prices allow them to maintain social contracts, invest in sovereign wealth funds for future generations, and pursue their own economic diversification plans.

- Major Oil Companies (Exxon, Shell, etc.): While not part of OPEC+, these international corporations benefit immensely. They sell the oil and gas they produce at these higher prices, leading to record profits and strong returns for their shareholders.

The Losers: The Import-Dependent World

The burden of higher prices falls disproportionately on nations that must import their energy.

- Developing and Emerging Economies: This is the hardest-hit group. Countries like India, Pakistan, Egypt, and many in sub-Saharan Africa are critically dependent on imported energy. A spike in oil prices devastates their trade balance—they have to spend more of their foreign currency reserves to pay for oil, weakening their national currency. This makes all their other imports more expensive, leading to spiraling inflation, social unrest, and difficult choices between funding fuel subsidies or other essential public services.

- Energy-Importing Developed Nations: While more resilient, countries in Europe and Asia (like Japan and South Korea) still face significant headwinds. Higher energy imports act as a tax on economic growth, reducing consumer spending power and corporate investment. The political pressure on governments to provide relief is intense.

- The Global Consumer: Ultimately, the cost is individual. For a middle-class family in the United States or Europe, higher energy costs act as a drain on disposable income, forcing trade-offs in the family budget. For low-income households, who spend a larger percentage of their income on essentials like fuel and food, the impact is crippling. It can mean choosing between heating and eating, between driving to work and paying a utility bill.

The Geopolitical Reckoning: Power Shifts and New Alliances

The OPEC+ decision is a profound exercise of geopolitical power. It demonstrates a significant shift in the global order, where traditional Western alliances are being challenged by new economic realities.

The Saudi-Russia Axis: The continued, robust cooperation between Saudi Arabia and Russia within OPEC+ is perhaps the most significant outcome. Despite pressure from its longtime security partner, the United States, Saudi Arabia has consistently chosen to align its energy policy with Moscow. This signals a move towards a more multipolar world where Middle Eastern powers are pursuing independent foreign policies based on economic self-interest rather than Cold War-era alliances.

The Diminishment of U.S. Influence: The U.S., now the world’s largest oil producer thanks to shale, has less direct leverage over global oil prices than in the past. While it can increase its own production (a slow process), it cannot command other nations to do so. The Biden administration’s failed attempts to persuade Saudi Arabia to pump more oil highlighted this new reality. The weaponization of energy policy is no longer a tool solely available to the West.

Energy as a Strategic Weapon: OPEC+’s action shows that energy supply can be used as a non-kinetic tool of statecraft. By managing supply to achieve a desired price, these nations can influence the economic health and policy decisions of their rivals and customers alike, granting them a form of soft power that is difficult to counter.

The Green Energy Paradox: A Complicated Relationship

The intuitive assumption is that high oil prices are a boon for renewable energy and electric vehicles (EVs). The reality is far more complex and paradoxical.

The Bull Case for Renewables:

- Improved Economics: High gasoline prices make electric vehicles more attractive on a cost-per-mile basis. High natural gas prices (often correlated with oil) make wind and solar power more cost-competitive for electricity generation.

- Energy Security Imperative: For importing nations, price spikes reinforce the strategic need to invest in domestic renewable energy sources to achieve independence from volatile global markets.

- Consumer Shift: Sustained high prices can permanently alter consumer behavior, encouraging more use of public transport, adoption of efficient vehicles, and overall conservation.

The Bear Case and Complications:

- Inflationary Headwinds: High oil prices drive up inflation, which forces central banks to raise interest rates. Renewable energy projects are extremely capital-intensive. Higher financing costs can delay or cancel gigawatts of new wind and solar installations, ironically slowing the energy transition.

- Political Backlash: Soaring energy costs can create a political environment hostile to climate policies. Voters struggling with bills may reject carbon taxes or support politicians who promise to “drill, baby, drill,” locking in more fossil fuel infrastructure for decades.

- The Petrostate’s Advantage: High oil prices fill the coffers of petrostates, giving them more resources to invest in their own energy transition. Saudi Arabia, for instance, is using its oil wealth to become a world leader in green hydrogen and solar power, ensuring it remains an energy superpower in a post-carbon world.

The relationship is not linear. High prices can simultaneously accelerate adoption by consumers while creating macroeconomic conditions that hinder large-scale industrial deployment of alternatives.

The Road to 2026: Navigating a Landscape of Uncertainty

The OPEC+ plan provides a framework, but the path to 2026 is fraught with variables that could derail its strategy or amplify its effects.

1. The Recession Wild Card: The biggest threat to OPEC+ is a severe global recession. If the central banks’ medicine works too well and crushes economic demand, the need for oil could plummet. A deep recession could create a oil glut so large that even extended cuts would be insufficient to hold prices up, causing a collapse in revenue—the very outcome the cuts were designed to prevent.

2. The U.S. Shale Response: The key question is how U.S. shale producers will react. Higher prices typically trigger more drilling. However, the industry has changed. After a decade of boom-bust cycles, producers are under intense pressure from shareholders to prioritize profitability and debt reduction over growth. They may not ramp up production as quickly as they have in the past. Nevertheless, the Permian Basin in Texas remains the world’s most prolific oil field, and its output will be a critical factor in balancing the market.

3. Chinese Demand: China is the world’s largest oil importer. The health of its economy is the single most important factor for global oil demand growth. A prolonged property crisis or weak consumer spending there would significantly dampen demand, overwhelming OPEC+’s efforts to tighten the market.

4. Geopolitical Black Swans: The oil market is perpetually one major disruption away from a price explosion. An escalation of conflict in the Middle East that threatens the Strait of Hormuz (a chokepoint for 20% of the world’s oil), a hurricane season that cripples U.S. Gulf Coast production, or a further major disruption to Russian exports could send prices soaring far beyond $100 a barrel, creating an entirely different set of economic and political crises.

5. The Pace of Transition: Technological breakthroughs in battery technology, renewable energy storage, or energy efficiency could accelerate the transition away from oil faster than OPEC+ anticipates, permanently eroding demand and making their vast reserves less valuable—a phenomenon known as “stranded asset risk.”

A Guide for the Consumer: Navigating the New Energy Reality

For individuals, the macro-economic shifts can feel overwhelming and beyond control. However, understanding the forces at play empowers smarter personal and financial decisions.

- Budget for Energy Volatility: The era of stable, cheap energy is likely over. Incorporate a higher and more flexible line item for transportation and home energy costs into your long-term budget.

- Prioritize Efficiency: If you are in the market for a vehicle, fuel efficiency should be a primary consideration. For homeowners, investments in insulation, energy-efficient windows, and smart thermostats offer a higher return than ever before, acting as a hedge against future price spikes.

- Understand the Ripple Effect: Be aware that the cost of nearly every good and service is linked to energy. This awareness can lead to more mindful consumption and spending choices.

- Evaluate Long-Term Investments: For those considering solar panels or an electric vehicle, a future of high and volatile fossil fuel prices significantly improves the financial calculus and shortens the payback period for these investments.

- Advocate for Policy: On a civic level, understanding this dynamic highlights the importance of supporting policies that promote energy independence through diversification, domestic renewable production, and investment in public transportation infrastructure.

Conclusion: The Unavoidable Interdependence

The decision by OPEC+ to extend its supply cuts is a powerful testament to the enduring centrality of oil in the global economy. It is a reminder that despite the undeniable momentum of the energy transition, the world still runs on hydrocarbons. The fortunes of nations, the stability of economies, and the balance of geopolitical power are still deeply tied to the price of a barrel of crude.

This move secures the fiscal health of producer nations but does so at a potential cost to global economic stability and the financial well-being of consumers worldwide. It underscores the urgent and complex challenge of navigating the path to a more secure and sustainable energy future—a path that is not just about environmental necessity but also about economic resilience and geopolitical independence.

The ripples from Vienna will continue to spread for years, a constant reminder of our deep and often vulnerable interdependence in a world still powered by fossil fuels. The road to 2026 will be a defining period, shaped by the choices of producers, the responses of consumers, and the unpredictable tides of the global economy.

0fdvqy

i6bmu3

Magnificent beat ! I wish to apprentice while you amend your site, how could i subscribe for a blog site? The account aided me a acceptable deal. I had been a little bit acquainted of this your broadcast provided bright clear idea

Hi there! This post couldn’t be written any better! Reading through this post reminds me of my previous room mate! He always kept talking about this. I will forward this article to him. Pretty sure he will have a good read. Thank you for sharing!

Good post. I study something more difficult on different blogs everyday. It is going to always be stimulating to read content from different writers and follow a bit something from their store. I’d want to use some with the content on my blog whether or not you don’t mind. Natually I’ll offer you a hyperlink in your net blog. Thanks for sharing.

Hello, you used to write fantastic, but the last several posts have been kinda boring… I miss your tremendous writings. Past few posts are just a bit out of track! come on!

This design is steller! You certainly know how to keep a reader entertained. Between your wit and your videos, I was almost moved to start my own blog (well, almost…HaHa!) Wonderful job. I really loved what you had to say, and more than that, how you presented it. Too cool!

This website is known as a stroll-through for the entire information you wanted about this and didn’t know who to ask. Glimpse here, and also you’ll definitely uncover it.

Saved as a favorite, I really like your blog!

Keep up the fantastic work, I read few blog posts on this internet site and I conceive that your website is real interesting and holds circles of superb info .

The other day, while I was at work, my sister stole my iphone and tested to see if it can survive a forty foot drop, just so she can be a youtube sensation. My iPad is now destroyed and she has 83 views. I know this is completely off topic but I had to share it with someone!

Merely wanna remark that you have a very decent internet site, I like the layout it really stands out.

Very well written story. It will be helpful to anybody who usess it, including myself. Keep up the good work – can’r wait to read more posts.

Hi my family member! I want to say that this article is awesome, great written and come with approximately all significant infos. I would like to peer more posts like this .

Thank you for sharing excellent informations. Your web site is very cool. I am impressed by the details that you¦ve on this site. It reveals how nicely you perceive this subject. Bookmarked this website page, will come back for extra articles. You, my pal, ROCK! I found just the information I already searched all over the place and simply couldn’t come across. What an ideal site.

**mitolyn reviews**

Mitolyn is a carefully developed, plant-based formula created to help support metabolic efficiency and encourage healthy, lasting weight management.

Great – I should definitely pronounce, impressed with your website. I had no trouble navigating through all the tabs and related info ended up being truly simple to do to access. I recently found what I hoped for before you know it in the least. Quite unusual. Is likely to appreciate it for those who add forums or anything, web site theme . a tones way for your customer to communicate. Excellent task..

Well I really enjoyed reading it. This information provided by you is very helpful for accurate planning.

Very nice info and right to the point. I am not sure if this is really the best place to ask but do you folks have any thoughts on where to hire some professional writers? Thanks 🙂

Your point of view caught my eye and was very interesting. Thanks. I have a question for you. https://www.binance.com/sl/register?ref=GQ1JXNRE

The next time I read a blog, I hope that it doesnt disappoint me as much as this one. I mean, I know it was my choice to read, but I actually thought youd have something interesting to say. All I hear is a bunch of whining about something that you could fix if you werent too busy looking for attention.