Part One: The Window

Imagine a busy government building in the heart of any American city. It is a Tuesday morning in April. The rain is coming down hard. Outside one door, a line stretches around the block. Inside that line, you see nurses, truck drivers, teachers, construction workers, and cashiers. They are holding W-2 forms in their cold hands. They look tired. Many of them worked overtime last month just to afford the bills. Now, they are here to pay their share.

Outside another door, just fifty feet away, there is a second line. This line is short. Only a few people stand there. They are dressed in clean coats and nice shoes. One of them is checking stock prices on his phone. Another is talking about the sale of a rental property. These people are investors.

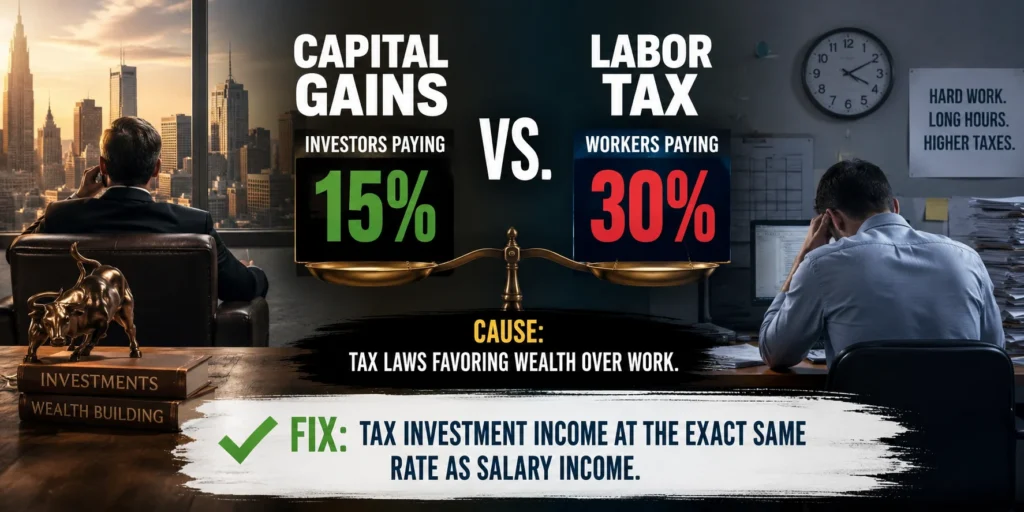

Here is the secret that the building does not advertise: The people in the first line will pay nearly 30% of every new dollar they earned last year. The people in the second line will pay only 15% of every new dollar they earned.

That is not a typo. The nurse who held a dying patient’s hand pays twice as much of her income to the government as the investor who simply owned shares of the hospital company.

This story is not about rich vs. poor, exactly. It is about work vs. money. It is about a tax code that has quietly decided that your time is worth less than your capital.

Let us walk through the history, the math, and the solution to one of the most hidden imbalances in modern America: Capital gains tax rate vs labor tax rate.

Part Two: Meet Maria and Robert (A Story of Two Incomes)

To understand the problem, you need two people.

Maria is a single mother. She works as a licensed practical nurse at a rehabilitation center in Ohio. She wakes up at 5:00 AM, makes breakfast for her son, and drives 30 minutes to work. She lifts patients, cleans wounds, and deals with stressed families. Last year, her base salary was $55,000. But because of a staffing shortage, she worked 10 hours of overtime every week. That pushed her total earnings to $68,000.

Robert lives two towns over. He is 58 years old. He retired five years ago after selling a small chain of dry-cleaning stores. He does not work anymore. But he has $1.2 million invested in the stock market—a mix of tech stocks, real estate investment trusts, and bonds. Last year, the market did well. He sold some shares of a software company that he had bought ten years earlier. His profit from that sale was $68,000. No overtime. No patients. No 5:00 AM alarm. Just a few clicks on his laptop.

Both Maria and Robert made exactly $68,000 from January to December.

Now, let us look at what happens on tax day.

Maria’s Tax Bill (Labor Income)

- Total wages: $68,000

- Standard deduction (single filer, 2025 approx): -$14,600

- Taxable income: $53,400

She falls into the 22% federal income tax bracket for most of her money. But wait—she also pays Social Security (6.2%) and Medicare (1.45%) on every dollar she earned. That is an extra 7.65%.

So her real federal tax rate on that $68,000 is not just 22%. It’s 22% + 7.65% = 29.65% on the bulk of her earnings. After state taxes (say Ohio’s flat rate of about 3%), she is pushing 33% total.

From her $68,000, Maria keeps roughly $45,000. The government takes about $23,000.

Robert’s Tax Bill (Capital Gains Income)

- Long-term capital gains: $68,000 (he bought the stock for $100,000 and sold for $168,000)

- Standard deduction: He uses it against any other income, but capital gains sit on top.

- Special rate for long-term gains: 0% up to about $47,000 of total income for a single person. Then 15% on the rest.

Robert’s $68,000 in gains: He pays 0% on the first $47,000 (yes, zero). He pays 15% on the remaining $21,000. That is about $3,150 in federal taxes.

No Social Security tax. No Medicare tax. No payroll tax.

Total federal tax for Robert: ~4.6% effective rate.

Let me write that again.

- Maria (worker): ~30%

- Robert (investor): ~4.6% to 15% at most

Robert keeps over $64,000. Maria keeps $45,000.

They made the same $68,000. But because Maria’s money came from sweat and Robert’s money came from shares, the law gave Robert a gift worth nearly $19,000.

That is the capital gains vs labor tax gap.

Part Three: How Did This Happen? A Short History

The tax code was not always this lopsided.

Before 1921, capital gains were taxed just like regular income. If you were a farmer selling land or a factory owner selling machinery, you paid the same rate as your workers. But after World War I, wealthy investors complained that high wartime tax rates (over 70% on top incomes) made them afraid to sell assets. They said: “Why would I sell my stock and pay 70%? I will just hold onto it forever. That means no tax revenue for the government.”

Congress listened. In 1921, they created a special lower rate for capital gains. The logic was: Lower taxes on investment income will encourage people to sell and reinvest, which helps the economy.

That idea became holy scripture in Washington.

Over the next 100 years, the gap grew. In the 1970s, the top labor tax rate was 70% while the capital gains rate was 39%. Still a gap. In the 1980s, Ronald Reagan lowered both, but the gap remained. In 2003, George W. Bush pushed the long-term capital gains rate down to 15%. Barack Obama kept it there. Donald Trump kept it there. Joe Biden tried to raise it for people making over $1 million, but Congress did not pass it.

Today, the top labor rate for a high earner is 37% + 3.8% (Net Investment Income Tax) + payroll = over 40%. The top capital gains rate is 20% + 3.8% = 23.8%.

For middle earners like Maria, labor tax is ~30% and capital gains is 15% or 0%.

The law has a clear favorite. And it is not the nurse.

The Quiet Year That Changed Everything: 1986

Most people do not know about 1986. That was the year Congress came closer than ever to fixing the gap. The Tax Reform Act of 1986 was a bipartisan monster of a bill. It lowered the top labor rate from 50% to 28% and raised the capital gains rate from 20% to 28%. For one brief shining moment, the two rates were equal.

Yes, for a short time in the late 1980s, a CEO and a stock trader paid the same top rate on their income. It was not perfect. Payroll taxes still favored investors. But it was close.

Then what happened? In 1990, President George H.W. Bush raised labor rates slightly but kept capital gains at 28%. In 1993, Bill Clinton raised the top labor rate to 39.6% but left capital gains at 28%—the gap returned. In 1997, Clinton actually cut capital gains to 20% while labor stayed high. The gap grew again. By 2003, the gap was a canyon.

The lesson of 1986 is simple: Equality is possible. We have done it before. We just chose not to keep it.

Part Four: The Three Arguments That Defend the Gap

You might be thinking: “There must be a good reason. Otherwise, why would we keep this?”

Let me present the three most common arguments from defenders of the lower capital gains tax. Then we will test each one against reality.

Argument #1: “We are taxing inflation, not real profit.”

The idea: If you bought a house for $200,000 and sold it 20 years later for $300,000, some of that $100,000 “profit” is just the dollar losing value. They say that taxing the whole gain is unfair.

Reality: True, inflation eats into real gains. But that is also true for wages. If Maria gets a 3% raise but inflation is 3%, her real income did not change—yet she still pays full income tax on that raise. Investors get a special inflation excuse. Workers do not. Also, the government already has a tool for inflation called “indexing.” We could easily adjust capital gains for inflation without giving a permanent discount. But we don’t. We just give the discount across the board.

Argument #2: “Lower capital gains taxes encourage investment.”

The idea: If you tax stock sales too high, people will not sell. They will hoard cash or buy gold. That freezes the economy.

Reality: Investment happens when companies have good ideas and customers have money. The stock market boomed in the 1950s and 1960s when capital gains rates were 25% and labor rates were 90%. Investment did not die. Also, most big investors are not day-trading their retirement. They invest for the long term regardless of the tax rate, because the alternative (not investing) loses to inflation. A 2021 study by the London School of Economics looked at 30 years of data across 18 countries. It found no consistent link between lower capital gains taxes and higher economic growth. None.

Argument #3: “We already taxed that money once as corporate income.”

The idea: When a corporation makes a profit, it pays corporate tax (21%). Then when you get a dividend or sell stock, you pay capital gains. That is “double taxation.”

Reality: Wages are also “double taxed” in a way. Maria’s employer pays payroll taxes (7.65%) before she ever sees her paycheck. Then she pays income tax. Then she pays sales tax when she buys groceries. Every dollar is taxed many times. Only investment dollars get special sympathy. Also, many capital gains come from assets that were never corporate profits—like your personal home, a piece of art, or cryptocurrency mining. Why should those get the same discount?

None of these arguments hold up when you compare them to the life of a worker.

Part Five: The Hidden Cost of the Gap (Not Just Money)

The damage is not only that Maria pays more. The damage is what the gap does to American behavior.

When the tax code punishes work and rewards waiting, people make strange choices.

- A young doctor thinks: “Why work 80 hours a week if the tax man takes 40%? Maybe I should just invest my family’s money instead.”

- A small business owner decides not to hire a new employee, because payroll taxes are high, but she will buy $100,000 of Apple stock—no taxes until she sells.

- A retiree with $5 million in the market pays 15% on his gains while his grandson pays 20% on his part-time job at Pizza Hut.

Over time, the economy shifts. More money flows into passive assets (stocks, bonds, real estate). Less money flows into active work (building things, caring for people, teaching kids).

We are not surprised when a country that taxes work lightly and investment heavily has lots of entrepreneurs. But America does the opposite. We tax work heavily and investment lightly. So we get lots of stock trading and less small business formation than we could.

The Psychological Toll on Workers

There is another cost that numbers cannot capture. It is the feeling of being played for a fool.

Maria does not need a degree in economics to notice that her brother-in-law, who inherited $400,000 and never worked a day in his life, pays less tax on his stock sales than she pays on her overtime. She feels it in her gut. She feels the unfairness when she looks at her paycheck and sees the deductions for Social Security, Medicare, federal withholding, and state tax. Then she hears that millionaires pay a lower rate on their investment income.

That feeling erodes trust. Trust in the government. Trust in the system. Trust in the idea that America is a place where everyone plays by the same rules.

When people stop believing the rules are fair, they start cheating. They hide income. They work under the table. They stop caring about paying taxes at all. That hurts everyone.

According to a 2023 survey by the Pew Research Center, 68% of Americans believe the tax system favors the wealthy. That is up from 55% ten years ago. The capital gains preference is the number one reason given when people are asked to explain why they feel that way.

Part Six: What Would Equal Treatment Look Like?

Now we come to the fix. It is simple to say, but politically hard to do:

Tax all income—whether from wages or from the sale of assets—at the exact same progressive rates.

That means:

- Eliminate the special “long-term capital gains” rate. All capital gains become ordinary income.

- Keep the standard deduction and progressive brackets. So a retired investor with $40,000 in gains pays 0% (same as a worker with $40,000 in wages).

- Keep the preferential treatment for retirement accounts (401k, IRA). Because those are already tax-deferred or tax-free. Do not disturb that.

- Adjust for inflation using a “chained CPI” method so that you only tax real gains above inflation. This is the one fair concession to the inflation argument.

What would that mean for Maria and Robert?

- Maria: No change. She still pays ~30%.

- Robert: Instead of paying 15% on part of his $68,000 gain, he would pay the same brackets as Maria. After the standard deduction, his taxable gain would be $53,400. That falls in the 22% bracket. He would pay about $11,750 in federal tax, plus state tax.

Robert would still be rich. He would still have over $56,000 after tax. But Maria would not be paying nearly double the rate.

That is fairness.

A Deeper Dive: The Progressive Rate Structure

Some people worry that making capital gains “ordinary income” means a billionaire could pay 37% on a stock sale. That is true. But let’s be honest: that billionaire paid 15% on the same sale under current law. Is 37% too high? Maybe. But is 15% too low? Almost certainly.

A truly fair system might have a middle path. For example:

- First $50,000 of capital gains per year: taxed at 0% (protects small savers)

- Next $100,000: taxed at 15% (lower than labor)

- Anything above $150,000: taxed at ordinary labor rates (22%, 24%, 32%, 35%, 37%)

That is called a progressive capital gains tax. Several members of Congress have proposed versions of this. It keeps the benefit for middle-class families selling a home or cashing out a small 401k. It raises rates only on large gains—the kind that only wealthy investors have.

But even that compromise is controversial. The purest version—full equality—is the cleanest.

Part Seven: But Won’t That Crush the Stock Market?

This is the fear that stops every reform. Politicians say: “If you raise taxes on capital gains, old people will sell stocks in panic, and the market will crash.”

Let’s look at the evidence.

In 1986, Congress passed a major tax reform. They raised the capital gains rate from 20% to 28% (making it equal to ordinary income for top brackets). What happened to the stock market in 1987? It went up 5% in the first half of the year. Then there was a crash in October 1987—but most economists blame new computer trading programs, not the tax change. By 1989, the market had fully recovered and doubled from its 1982 lows.

In 2013, President Obama raised the top capital gains rate from 15% to 20% (plus a 3.8% surcharge for high earners). The S&P 500 went up 30% that year.

In 1997, Congress cut the capital gains rate from 28% to 20%. The market went up, but also crashed in 2000. Tax rates alone do not drive markets. Profits, interest rates, and human psychology drive markets.

The truth: Investors will not stop investing if the tax rate is fair. They will simply adjust. They might hold stocks longer. They might prefer tax-free municipal bonds. But they will not stuff cash under mattresses.

What About the “Lock-In Effect”?

Economists talk about a “lock-in effect.” That means if you raise taxes on capital gains, people will refuse to sell their assets. They will hold them until death. Then their heirs get a “step-up in basis” (meaning the tax liability disappears). So the government gets nothing.

This is a real problem. But the solution is not to keep rates low forever. The solution is to close the step-up loophole. If you eliminate step-up in basis for estates over $5 million, then people have no reason to hold forever. They will sell, pay the tax, and move on.

A few simple reforms can fix the lock-in effect without keeping the current 15% rate.

Part Eight: The Human Side of the Math

Let me tell you about my uncle Frank. Frank worked in a furniture factory for 38 years. He never made more than $22 an hour. When he retired, he had a small pension and a 401k with about $180,000. He did not think of himself as an “investor.” But the tax code did.

In his first year of retirement, he needed extra money to fix his roof. He sold $15,000 worth of mutual fund shares that he had bought 20 years earlier. His gain was about $9,000. He paid 0% federal tax on that gain because his total income was low.

Now compare that to my neighbor, Darrell. Darrell is a plumber. He works 50 hours a week. He earns $75,000. He pays about 22% federal plus 7.65% payroll. On his last $1,000 of overtime, he keeps about $700.

Frank paid nothing on his $9,000 gain. Darrell paid 30% on his overtime.

Who needs the break more? The retired factory worker with a paid-off house and Social Security? Or the plumber with two kids in daycare?

Most people, if you ask them honestly, would say Darrell. But the tax code says Frank.

That is the quiet injustice of the capital gains preference. It is not only about billionaires. It is about the structure: unearned income gets a discount. Earned income pays full price.

A Family Story: The Martinez Family

Let me tell you about another family. The Martinezes live outside Phoenix, Arizona. Elena Martinez works as a receptionist at a dental office. Her husband Carlos drives a delivery truck for a beverage company. Together, they earn $92,000 a year. They have two kids. They pay about 22% of their income to federal taxes after deductions, plus 7.65% payroll, plus Arizona state tax of about 4%. Their effective total tax rate is around 30%.

Now consider Elena’s father, Mr. Gutierrez. He is 72. He worked as a janitor for 40 years. He saved carefully and bought a small apartment building with three units. He lives in one and rents the other two. Last year, he sold the building for a profit of $180,000. He had owned it for 25 years.

Under current law, Mr. Gutierrez pays 0% on the first $47,000 of that gain, then 15% on the rest. His total federal tax on the $180,000 is about $20,000. That is an effective rate of 11%.

So Elena and Carlos pay 30% on their hard-earned wages. Mr. Gutierrez pays 11% on his building sale. The family loves Mr. Gutierrez. He is a good man. But is it fair that his unearned profit is taxed at one-third the rate of his daughter’s labor?

Most people, when you put it that way, say no.

Part Nine: What Other Countries Do (And What We Can Learn)

The United States is not alone in favoring capital gains. But we are more extreme than many peers.

Canada: Taxes 50% of capital gains as ordinary income. That means if you have a $10,000 gain, you add $5,000 to your income and pay your normal rate. Effective top rate on gains is about 27% vs 33% on labor. Small gap.

Germany: Has a flat 25% withholding tax on capital gains plus a solidarity surcharge. Labor taxes are progressive up to 45%. So a high earner pays 45% on wages and 25% on gains. Still a gap, but not as wide as the US.

United Kingdom: Capital gains taxed at 20% for higher earners, while labor income goes to 45%. Gap of 25 percentage points. Very similar to US.

New Zealand: No capital gains tax at all on most assets (except some property). Labor taxes up to 39%. That is a massive gap—and economists there are fighting over it now.

Belgium: Generally no capital gains tax on normal management of private wealth. Labor taxes are very high (50%+). Huge gap.

France: Has a flat 30% tax on capital gains (including social charges). Labor taxes are progressive up to 45%. So a high earner pays 45% on wages and 30% on gains. Gap of 15 points.

Sweden: Taxes capital gains at 30% flat. Labor taxes are progressive up to 57% (including local taxes). Gap of 27 points. Sweden is often seen as a high-tax country, but note: their capital gains rate is actually higher than the US rate for most people (30% vs 15-20%).

You see a pattern. Almost every developed country gives some break to investment income. But the US gap is among the largest when you factor in the 0% bracket for low and middle gains.

The countries with the smallest gaps (Canada, France) also have higher levels of economic mobility and less wealth concentration. That does not prove causation, but it is worth noticing.

A Closer Look at Canada

Canada’s system is instructive. Before 1972, Canada had no capital gains tax at all. Then they introduced one. Today, only 50% of a capital gain is included in taxable income. So if you have a $100,000 gain, you add $50,000 to your income and pay your marginal rate (which ranges from 15% to 33% federal, plus provinces). The effective top rate on gains is about 27%.

That means a Canadian investor with a $200,000 gain pays roughly $54,000 in tax. An American investor with the same gain pays 15% or $30,000. The Canadian pays almost twice as much. And yet, Canada’s stock market has performed similarly to the US market over long periods. Canadian startups still get funded. Canadian retirees still live comfortably.

The lesson: Higher capital gains taxes do not destroy an economy. They just make it a little more fair.

Part Ten: The Objections We Must Take Seriously

I have been arguing for equal rates. But any honest article must address the strongest counterarguments.

Objection 1: “Capital is mobile. If you tax it too much, it leaves the country.”

This is real. A wealthy investor can sell US stocks and buy Irish stocks or Singapore real estate. The solution is not to lower taxes forever in a race to the bottom. The solution is international cooperation (a global minimum tax, which over 130 countries have already agreed to in principle). Also, most investment income is from US real estate, US companies, and US bonds. You cannot move a skyscraper to Bermuda. You cannot move a US Treasury bond to the Cayman Islands. The vast majority of capital gains come from assets that are physically or legally tied to the United States.

Objection 2: “You will punish retirees who saved their whole lives.”

This is the most emotionally powerful argument. But remember: a retiree with $50,000 in total income from Social Security and small capital gains pays 0% on gains under the current system (because of the 0% bracket). Under an equal system, they would still pay 0% if their total income is low. The change would affect only retirees with large gains—over $47,000 in taxable income for a single person. That is not your grandma living on $30,000 a year. That is a wealthy retiree.

Also, we can protect small gains. The proposal I outlined earlier—a $10,000 annual exclusion—would mean that 90% of American households pay zero capital gains tax on their occasional stock sales. The change would hit only the top 10% of households by wealth. That is exactly where the tax code should be less generous.

Objection 3: “Savings are taxed when you earn them, then again when they grow.”

Yes, but that is also true for labor. You pay tax when you earn money, then you pay sales tax when you spend it, then property tax if you buy a house. The complaint about “double taxation” only applies to capital. That is special pleading.

Moreover, retirement accounts like 401(k)s and IRAs already avoid double taxation. The money goes in pre-tax, grows tax-free, and is only taxed when withdrawn as ordinary income. That is a fair system. The problem is with non-retirement investments—the ones used mostly by wealthy people.

Objection 4: “Higher capital gains tax will reduce startup investment.”

This is the most plausible concern. Angel investors and venture capitalists take huge risks. If you tax their gains at 40%, they might put money into safe bonds instead of new biotech firms. But note: most startup gains are already taxed as ordinary income because they are held for less than one year (short-term gains). The long-term rate applies after one year. A founder who works for three years to build a company and then sells—why should that reward be taxed less than a nurse’s salary? There is no good answer except “we have always done it this way.”

Also, many successful startup founders (like Elon Musk and Jeff Bezos) did not build their companies because of low capital gains taxes. They built them because they had a vision and a drive. Low taxes did not create Amazon. Hard work did.

Objection 5: “It will be too complicated.”

This is a classic dodge. Any change to the tax code requires new forms and new calculations. But equalizing rates is actually simpler than the current system. Right now, you have to track holding periods (short vs long term), calculate different rates (0%, 15%, 20%, plus the 3.8% surcharge), and deal with complex rules like “qualified dividends.” Under a flat equal system, you would just add your gains to your wages and use one tax table. That is simpler, not harder.

Part Eleven: The Simpler Fix (A Proposal You Can Understand)

We do not need a 2,000-page tax bill. We need three sentences.

Sentence 1: “For tax years beginning after December 31, 2025, the term ‘net capital gain’ shall have no effect. All gains from the sale or exchange of capital assets shall be treated as ordinary income.”

Sentence 2: “The Internal Revenue Code is amended to provide a 50% exclusion of capital gains up to $10,000 per year ($20,000 for joint filers) to protect small savers.”

Sentence 3: “The Secretary of the Treasury shall issue regulations to adjust the basis of capital assets for inflation using the Chained Consumer Price Index for all assets held longer than three years.”

That is it.

- Large gains: taxed like wages.

- Small gains (under $10k): half excluded (so effective rate is lower for casual sales).

- Inflation adjustment: fair for long-held assets.

This would raise roughly $800 billion over ten years according to Penn Wharton Budget Model (2023 estimate). It would reduce the gap between the richest 1% and the middle class by about 6%. And it would send a simple message: One dollar of income is one dollar of income.

A Step-by-Step Example of the Fix

Let’s apply the fix to a real person. Meet Susan. She is a teacher in Texas. She earns $60,000 a year. She also inherited some stock from her grandmother. This year, she sold $12,000 of that stock. Her gain was $7,000 (she bought it for $5,000 many years ago).

Under current law:

- Susan’s wages: $60,000

- Her capital gain: $7,000

- Because her total income ($67,000) is below the 15% threshold for gains, she pays 0% on the $7,000.

- Total tax: just on her wages.

Under the equal tax fix:

- Wages: $60,000

- Gain: $7,000 (but $3,500 is excluded because of the 50% exclusion on gains under $10k)

- Taxable gain: $3,500

- Total taxable income: $63,500

- She pays her normal bracket (say 12% on most of it).

Susan pays a little more tax—maybe $400 extra. But she also benefits from the inflation adjustment and the small-gain exclusion. For most middle-class families, the difference is tiny.

Now apply the fix to a wealthy investor. Meet Harold. He has $5 million in the market. This year, he sold $500,000 of stock with a gain of $300,000.

Under current law:

- Harold pays 20% (top rate) + 3.8% surcharge = 23.8% on most of the $300,000.

- Tax bill: about $71,000.

Under the equal tax fix:

- The first $10,000 of gain is half excluded. The remaining $290,000 is taxed as ordinary income.

- Harold is in the top bracket (37%).

- Tax bill: about $107,000 (plus state taxes).

Harold pays about $36,000 more. He will still have over $193,000 left from the sale. He will be fine. Meanwhile, that $36,000 extra can go toward schools, roads, or deficit reduction.

That is the trade. And it is a fair one.

Part Twelve: What You Can Do Tomorrow

You are one person. You cannot rewrite the tax code tonight. But you can change your own choices and your voice.

If you are a worker:

- Learn where your representatives stand on equalizing capital gains. Most Democrats favor raising the rate to 28-39%. Most Republicans favor keeping 15-20%. A few independents want full equality. Find yours.

- In your 401k, remember that those gains are already tax-deferred. Do not feel guilty. The problem is not your retirement. It is the billionaire selling $500 million in stock at 15%.

- Talk to your coworkers. Many people do not even know that capital gains are taxed differently. A simple conversation can open eyes.

If you are an investor:

- Consider that lower taxes on your gains come from higher taxes on nurses and truck drivers. Is that the society you want?

- You can still be an investor and support fair taxes. Warren Buffett (himself worth over $100 billion) has famously said: “My secretary pays a higher tax rate than I do. That is wrong.” You can join him.

- Look into “tax diversification.” Even if rates go up, you can still build wealth. The stock market does not collapse just because the tax rate changes.

For everyone:

- Ask one question at every town hall: “Why does unearned income from stock sales get a discount while earned income from work does not?”

- Share this article. The first step to fixing a hidden imbalance is to turn on the lights.

- Write a letter to your member of Congress. It does not have to be long. Say: “I support HR 1234 (or whatever bill equalizes capital gains). Please co-sponsor it.” One letter represents thousands of voters.

A Sample Letter You Can Use

Here is a template. Copy it, change the names, and mail it or email it.

Dear Representative [Name],

I am a voter in your district. I am writing to ask you to support equal tax treatment of capital gains and labor income.

Under current law, a nurse pays nearly 30% of her wages in federal taxes, while an investor pays only 15% on stock profits. That is unfair. Income is income, whether it comes from a paycheck or a stock sale.

Please co-sponsor legislation to tax long-term capital gains at the same rates as ordinary income, with a small exemption for low- and middle-income taxpayers.

Thank you for your service.

Sincerely,

[Your Name]

That letter takes five minutes. It costs nothing. And it is one of the most powerful tools you have.

Part Thirteen: The Final Comparison

Let me end where we began. The two lines at the government window.

On the left, the worker line. Maria is in that line. She has varicose veins from standing all shift. She smells like hand sanitizer and coffee. She is calculating in her head: “If I give 30% to taxes, I cannot afford the summer camp for my son. Do I cancel his dental checkup instead?”

On the right, the investor line. Robert is in that line. He is relaxed. He just came from a morning walk. He is thinking about which golf course to play next week. He will pay 15% of his gain, but really 0% on the first $47,000. He will book a vacation to Maine next month.

The law did not create Robert’s wealth. He worked hard earlier in life. Good for him. But the law did not have to make Maria’s path so much steeper.

We have a choice. We can keep pretending that a dollar from capital gains is different from a dollar from wages. Or we can say: No more. Equal is equal.

The fix is not radical. It is not socialist. It is not “soak the rich.” It is simply honest.

Tax what you earn from your time the same as what you earn from your money.

That is not left or right. That is fair.

Part Fourteen: A Deeper History (The Forgotten Debates)

To really understand the gap, you have to go back further than 1921. You have to go back to the founding of the income tax itself.

Before 1913, the United States had no permanent federal income tax. The government lived mostly on tariffs and excise taxes. That system was regressive—the poor paid a higher percentage of their income than the rich. Progressives demanded change. In 1913, the 16th Amendment was ratified, allowing Congress to tax income directly.

The first income tax was very progressive. The top rate was 7% on income over $500,000 (about $15 million today). Capital gains were taxed as ordinary income. No special rate.

But World War I changed everything. The government needed money fast. They raised the top rate to 77% by 1918. That is when the wealthy started complaining. They said they would not sell stocks or property if the tax was that high. They called it “confiscation.”

In 1921, Treasury Secretary Andrew Mellon (one of the richest men in America) argued for a lower capital gains rate. He got it. The rate dropped to 12.5% while the top labor rate stayed at 58%. The gap was born.

For the next 60 years, the gap widened and narrowed, but never disappeared. The Great Depression saw labor rates go up and capital gains rates go down. World War II pushed labor rates to 94% (yes, ninety-four percent) but capital gains stayed around 25%. The 1950s and 1960s were the golden age of American labor unions, but the capital gains preference remained.

The Tax Reform Act of 1969 tried to close the gap. It created a 50% maximum tax on earned income but left capital gains at 25%. That created a weird situation: a doctor could pay 50% on his salary, but a stock trader could pay 25%. The doctor started asking questions.

By 1978, Congress lowered the capital gains rate to 28% and then to 20% in 1981. The gap grew again. Then came 1986—the year of equality—followed by the slow creep back to the gap we have today.

The lesson of this long history is simple: The gap is not an accident. It is the result of a century of lobbying by wealthy investors. Every time the gap closes a little, the financial industry fights to open it again.

Part Fifteen: The Moral Argument (Beyond the Math)

We have spent a lot of time on numbers. Tax rates, brackets, exclusions, and inflation adjustments. But the real argument is not about math. It is about morality.

What is the purpose of a tax system? To raise money for public goods. But also to be fair. To treat people equally under the law.

When the tax code treats a dollar from capital gains better than a dollar from wages, it is making a moral statement. It is saying: “Money that already exists is more worthy than the effort required to create new money.”

That is backwards.

Think about it this way. Maria, the nurse, creates value every day. She helps people heal. She comforts the dying. She holds the hand of an old woman whose family lives far away. That is real work. That is contribution.

Robert, the investor, also creates value. When he buys a stock, he provides capital to a company. That company can expand and hire people. That is real, too.

But why should Robert’s contribution be taxed less? If anything, Maria’s work is more essential. Without nurses, the stock market does not matter. Without investors, nurses still need to be paid.

The tax code has it backwards. It rewards the passive and punishes the active.

A Thought Experiment

Imagine two identical twins. Twin A works as a teacher for 40 years. She earns $50,000 a year. She pays 30% in taxes. Over her career, she pays about $600,000 in taxes.

Twin B never works a day. He inherits $1 million from a relative. He invests it in the stock market. Over 40 years, his investments grow to $4 million. He lives off the gains. He pays 15% on his capital gains. Over his lifetime, he pays about $450,000 in taxes.

Twin A worked 80,000 hours as a teacher. Twin B did nothing. Yet Twin B paid less total tax.

Is that fair? Most people, when you put it that way, say no.

Part Sixteen: The Political Reality (Why Change Is Hard)

If the gap is so unfair, why hasn’t it been fixed? The answer is political power.

The financial services industry spends hundreds of millions of dollars every year on lobbying. According to OpenSecrets.org, the securities and investment industry spent over $2.5 billion on lobbying between 2010 and 2020. That is more than oil, gas, and pharmaceuticals combined.

Their message to Congress is simple: “Lower capital gains taxes help the economy. Raise them, and you will hurt retirees and kill jobs.”

That message is repeated so often that many politicians believe it. Even some Democrats are afraid to raise capital gains rates too much. They remember what happened to Walter Mondale in 1984. He proposed raising taxes, and he lost in a landslide. The lesson they took was: “Never raise taxes on investment.”

But that lesson is too simple. Bill Clinton raised taxes in 1993, including a small increase in capital gains rates for top earners. He won re-election in 1996. Barack Obama raised capital gains rates on high earners in 2013. He was not on the ballot, but Democrats did fine in the next election.

The real barrier is not voters. It is campaign contributions.

The Role of Retirement Accounts

There is another political barrier: retirement accounts. Millions of middle-class families have 401(k)s and IRAs. They benefit from the capital gains preference because their accounts grow tax-deferred. They do not pay capital gains tax at all until withdrawal, and then they pay ordinary income rates.

That means many middle-class voters do not feel the capital gains gap. They think: “I pay taxes on my wages. I pay taxes on my 401k withdrawals. What’s the problem?”

The problem is that most of the capital gains preference goes to the wealthy. According to the Congressional Budget Office, the top 1% of households receive 68% of the benefit of the lower capital gains rate. The top 10% receive 92%. The bottom 90% receive just 8%.

So the vast majority of Americans get almost no benefit from the 15% rate. But they think they do because they have a 401k. That confusion is intentional. The financial industry wants you to believe that a lower capital gains rate helps you. It doesn’t. It helps the people who own most of the stocks—the top 1%.

Part Seventeen: What the Experts Say

Not everyone agrees with me. Let me present a range of expert opinions.

The Left View (Elizabeth Warren, Bernie Sanders): Tax capital gains as ordinary income, no exceptions. Also add a wealth tax on fortunes over $50 million. The current system is a “rigged game” that favors the wealthy.

The Center-Left View (Joe Biden, Janet Yellen): Raise the top capital gains rate to 39.6% for people making over $1 million. Keep the 15% rate for everyone else. Also close the “step-up in basis” loophole.

The Center-Right View (Mitt Romney, Doug Holtz-Eakin): Keep capital gains lower than labor rates to encourage investment. But raise the rate from 15% to 20% or 25% as a compromise. Also index for inflation.

The Right View (The Wall Street Journal editorial board): Keep capital gains at 15% or lower. Any increase will hurt the economy. Labor taxes are too high, so we should lower labor taxes instead of raising capital gains.

The Libertarian View (Cato Institute, Reason Foundation): Abolish the income tax entirely and replace it with a consumption tax or a flat tax. Under a pure flat tax, all income (including capital gains) would be taxed once at a low rate.

I fall somewhere between the Center-Left and the Center-Right. I think full equality is the most honest approach, but I would accept a compromise: tax capital gains at 25% top rate, index for inflation, and eliminate step-up in basis. That would raise significant revenue while still leaving a small preference for investment.

Part Eighteen: A Day in the Life After Reform

Let me paint a picture of what the world could look like if we fixed the gap.

It is 2030. Maria is still a nurse. She makes $78,000 now. Her son is in high school. She pays 25% total federal tax on her wages (down slightly because the new revenue from capital gains allowed a small payroll tax cut).

Robert is still retired. He sold another $68,000 in stock this year. Under the new law, he pays the same 22% bracket as Maria. His tax bill is $11,750. He still has plenty of money for his golf vacation. But he also notices that the local elementary school got a new roof because of the extra tax revenue.

The stock market did not crash in 2026 when the law passed. It dipped for a week, then recovered. Companies still invested. Startups still got funded. The world did not end.

And every April, when Maria stands in line at the government building, she no longer sees a separate line for investors. There is just one line. Everyone pays the same rate on every dollar of income.

She feels better. Not because she loves paying taxes, but because she believes the rules are fair.

That is the real goal. Not to punish the rich. Not to reward the poor. Just to make the rules the same for everyone.

Part Nineteen: Frequently Asked Questions

Let me answer some common questions you might still have.

Q: Does this apply to my home sale?

A: Currently, you can exclude up to $250,000 ($500,000 for married couples) of gain from the sale of your primary home if you have lived there two of the last five years. That exclusion would remain under almost every reform plan. So selling your home would still be tax-free for most people.

Q: What about dividends?

A: Dividends are currently taxed at the same 0/15/20% rates as capital gains. Under the fix, qualified dividends would be treated as ordinary income. That is fair because a dividend is just a profit distribution—it’s income.

Q: What about cryptocurrency?

A: Crypto is already treated as property. So gains from selling Bitcoin or Ethereum are capital gains. Under the fix, they would become ordinary income. This might actually help small crypto traders because they can use capital losses to offset wages.

Q: Won’t this hurt charitable giving?

A: Possibly. Some people donate appreciated stock to avoid paying capital gains tax. Under the fix, they would still get a deduction for the full fair market value. The deduction might be worth slightly less if their tax rate is higher, but most studies show that charitable giving is not very sensitive to tax rates.

Q: What about carried interest?

A: That is a separate loophole that allows hedge fund and private equity managers to treat their fees as capital gains. That loophole should be closed regardless of what happens to the general capital gains rate. Most reform plans include closing carried interest.

Q: Is this constitutional?

A: Yes. The 16th Amendment gives Congress the power to tax income “from whatever source derived.” The Supreme Court has repeatedly upheld the taxation of capital gains as income.

Part Twenty: The Last Word

We have traveled a long road together. From the two lines at the government window to the history of 1921, from Maria and Robert to the tax systems of Canada and Germany. We have looked at objections, weighed evidence, and proposed a simple fix.

Now it is your turn.

You know the secret. You know that a nurse pays 30% and an investor pays 15%. You know that this gap is not an accident. It is a choice. And choices can be unmade.

The next time you hear a politician say “we need to lower taxes on job creators,” you can ask: “What about the nurse who creates care? What about the teacher who creates educated children? Why is their labor worth less than a stock trade?”

The next time you file your own taxes, you can notice the line for capital gains. You can remember that this line represents a preference for wealth over work.

And the next time you vote, you can vote for someone who promises to make the rates equal.

One dollar. One rate. One line.

That is the fix. That is the future.

Let’s build it.